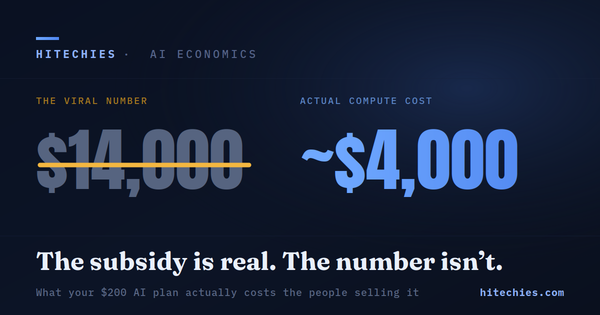

Before the hard questions — the company is real, the growth is real, and the mission matters more now than when Anthropic was founded. But at $900 billion, you deserve the full picture before October.

First, What Is Genuinely Extraordinary

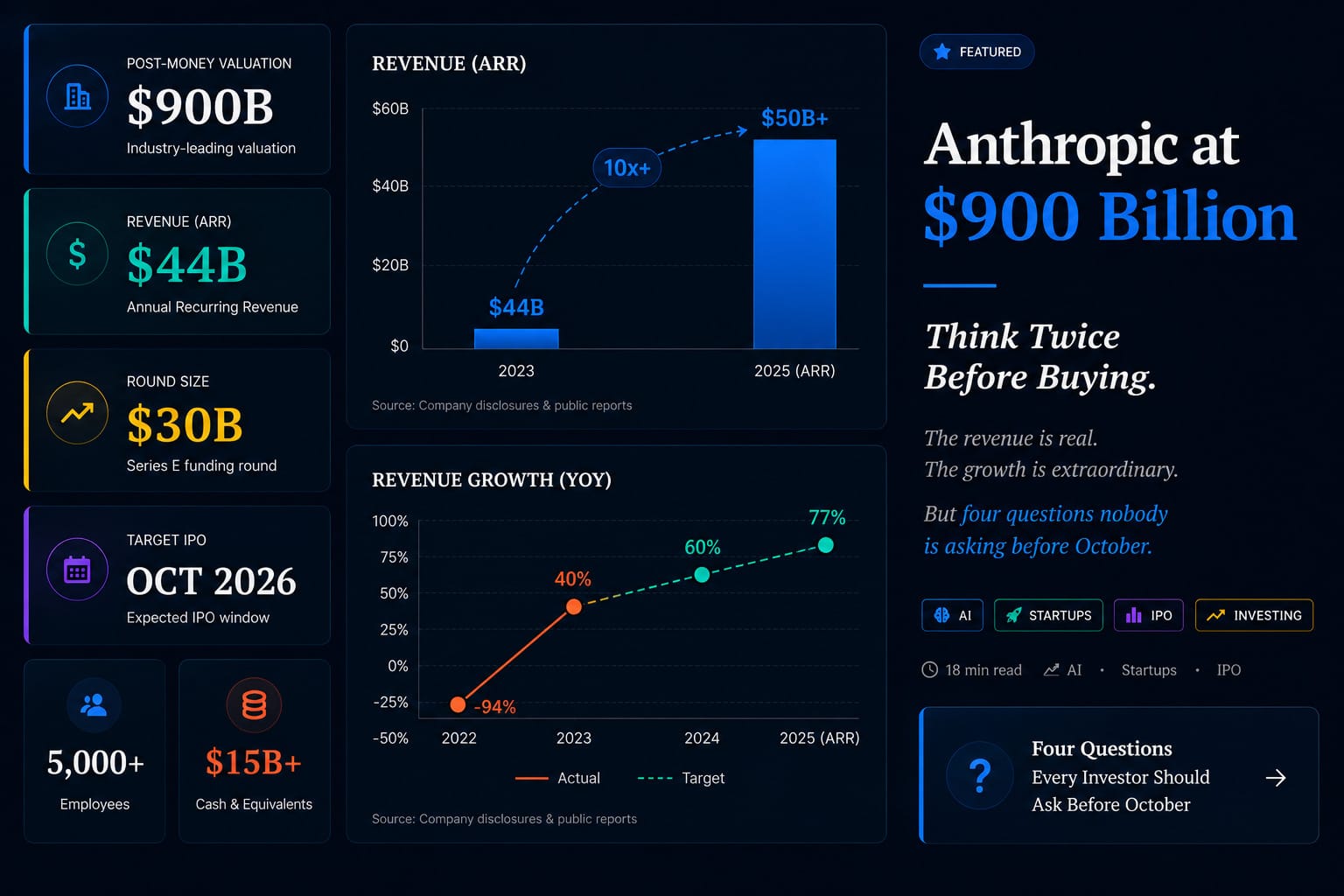

Salesforce took 20 years to reach $30 billion in annual revenue. Anthropic did it in under three years from zero. Dario Amodei described the growth himself as "crazy" — they planned for 10x annual growth and saw 80x.

Claude Code — the company's agentic coding product — became the fastest-growing enterprise software product in history. It went from launch in May 2025 to $1 billion in annualised revenue by November 2025. Eight of the Fortune 10 are customers. Over 1,000 companies are spending more than $1 million per year.

| Date | Revenue Run Rate | Change |

|---|---|---|

| Jan 2024 | $87 million | — |

| Dec 2024 | $1 billion | +1,050% |

| End 2025 | $9 billion | +800% |

| Feb 2026 | $14 billion | +56% |

| Mar 2026 | $19 billion | +36% |

| Apr 2026 | $44 billion | +132% |

| Jun 2026 (proj.) | $50 billion+ | Projected |

And the efficiency number that does not get enough attention: Anthropic has approximately 5,000 employees generating $44 billion in revenue. That is $8.8 million per employee. Nothing in enterprise software history comes close.

Question 1: Why Are They Selling Shares Now?

When a company raises money or sells shares, the first question is always: why now, and who benefits?

Anthropic has extraordinary momentum, the IPO window is open, and the capital will fund the next phase of infrastructure and research.

Google came in at roughly a $4 billion valuation. Amazon at similar levels. They are sitting on 100–200x paper gains they cannot touch until there is a liquid market. The IPO creates that market. Early investors need an exit — and the window is open right now.

There is also a timing calculation that has nothing to do with operational readiness. A recession, a major AI safety incident, a Chinese lab releasing a model that matches Claude at a fraction of the compute cost — any of these could close the window. October 2026 was chosen because the window is open, not because the business is optimally positioned for public scrutiny.

Pre-IPO shares were trading at approximately $1,447 per share in May 2026 — implying a valuation at or above $1 trillion. If the IPO prices at $900 billion, secondary market investors are already underwater on the open price.

Question 2: Is the $900 Billion Real?

The most sophisticated critique of this valuation has a sharp edge: "This is being valued like a future monopoly before the market structure even exists."

The bull case: if Anthropic hits $100 billion in annualised revenue by end of 2026 — which its own trajectory suggests is plausible — the $900 billion valuation implies roughly 9x forward revenue. At that point it looks reasonable. Anthropic also generates $2.10 of revenue per compute dollar spent, versus OpenAI's $1.60.

The deeper issue: we do not actually know what kind of company Anthropic is. If it is a software company, 20x revenue is aggressive but defensible. If it is an infrastructure company — burning capital on compute, locked into $15 billion annual hardware commitments — then the multiple that applies is closer to a data centre operator than a software firm. Data centre operators do not trade at 20x. They trade at 4x.

We are privatising infrastructure-level intelligence into a tiny number of corporations.

— A recurring critique from market concentration analystsQuestion 3: Will It Actually Be Profitable?

Anthropic is projecting its first profitable quarter in Q2 2026. That is a real milestone. But the most important detail about that profitability has received almost no coverage this week.

Anthropic's Q2 2026 profitability is being announced during the precise months when its SpaceX Colossus compute contract is at a discounted introductory rate as it ramps up. At full price, that contract costs $1.25 billion per month — $15 billion per year. Q3 2026, the first full-price quarter, is the real test.

The gross margin story is also more complicated than the headline suggests. In 2024, Anthropic's gross margin was negative 94% — spending nearly twice what it earned serving customers. In 2025 it improved to approximately 40% — but that was already 10 percentage points below the internal target, because inference costs came in 23% higher than anticipated. The 2028 target of 77% assumes one of the most aggressive margin expansion trajectories ever embedded in a private technology valuation.

Inference costs have fallen 90% year over year. With only 5,000 employees and $44B in revenue, the headcount cost base is extraordinary. If compute costs continue falling and enterprise revenue keeps growing as a share of the total, the margin story can absolutely reach 77% by 2028.

Question 4: What Happens to Safety When Quarterly Earnings Start?

This is the question that started the whole company. And the one that gets the least airtime in the funding coverage this week.

Anthropic was founded on the belief that AI safety and commercial success could coexist. The IPO puts that thesis under the most intense test it has ever faced. Public shareholders demand growth every 90 days, on earnings calls, in analyst notes, in the instant feedback of a stock price. Safety frameworks slow deployment. Slower deployment can mean losing market share.

Some academics argue directly: "You cannot simultaneously optimise for public-market hypergrowth and maximum caution."

Anthropic's governance structure — including its Long-Term Benefit Trust and public benefit corporation status — was designed to protect the safety mission from exactly this pressure. But the practical reality of being a public company has a way of eroding commitments that seemed ironclad in private. None of these structures have been tested against sustained quarterly earnings pressure. We simply do not know yet.

The Five Structural Risks (Stated Plainly)

The Hyperscaler Dependency Paradox

Amazon and Google are Anthropic's largest investors, largest infrastructure suppliers, and primary distribution channels. They also have their own competing models. Anthropic risks becoming an "AI feature supplier rather than a platform owner" — valued like independent infrastructure it does not fully control.

Medium-term riskThe Profitability Timing Question

Q2 2026 profitability is announced during discounted SpaceX compute rates. Full price kicks in at $1.25B/month. Q3 2026 is the real test. The S-1 will need to show whether profitability holds or Q2 was a carefully timed story.

Watch closelyOpen Source Pressure Is Accelerating

DeepSeek and Meta Llama are closing the gap to frontier performance fast, putting sustained downward pressure on commercial model pricing. A company with $15B in annual compute costs and 40% gross margins has very little pricing power to give up.

High long-term riskIs Enterprise Revenue Actually Durable?

Critics note much of current enterprise AI spending may still be experimentation budget. Switching costs between models remain low. Reuters noted major companies have begun reassessing AI spending as costs rise. The stickiness question remains unanswered.

Monitor in S-1AI Concentration Risk

If Anthropic and OpenAI both IPO at near-$1 trillion valuations, passive index funds will be forced to hold them automatically. Systemic exposure to a single technological sector controlled by a handful of executives will be at historic highs. Brussels, Washington, and Beijing are watching.

Regulatory exposureThe Honest Verdict

Anthropic is probably one of the most important technology companies in the world. The product is excellent. The growth is real. The mission matters. But the $900 billion valuation prices in a future where almost everything goes right.

Bull Case

- ↑$44B ARR growing at extraordinary pace

- ↑8 Fortune 10 companies as customers

- ↑Inference costs down 90% YoY

- ↑5,000 employees — elite efficiency

- ↑First profitable quarter Q2 2026

- ↑Only model on AWS + Google + Azure

Bear Case

- ↓20x revenue vs Microsoft's 12x

- ↓Q2 profitability on discounted rates

- ↓Open source closing capability gap

- ↓$15B/year compute bills

- ↓Safety mission vs. quarterly earnings

- ↓No audited public financials yet

The smartest way to get Anthropic exposure without full IPO risk? Amazon and Google. Both invested billions. Both profit from every Claude query. Both trade at single-digit revenue multiples. If Anthropic wins, they win. If Anthropic's valuation corrects, you are cushioned.

⚡ What to Watch Before the IPO

As of May 27, 2026, the $30B round has not been officially confirmed closed. No S-1 has been filed with the SEC. All revenue figures are company-disclosed annualised run rates, not audited financials. This is editorial analysis, not investment advice. Speak to a qualified financial advisor before making investment decisions.

Sources: Bloomberg, CNBC, Sacra, The Information, SaaStr, Seeking Alpha, Investing.com, Where's Your Ed At, Financial Times, Reuters, TechInformed.