The "AI that makes you rich while you sleep" ad isn't a dumb scam for dumb people. It's an industrialized operation that took billions last year, and in its worst form runs on trafficked labour. Here's how it works, how it differs from the real thing, and how to spot the fake in ten seconds. With sources, so you can check me.

A businessman in Hyderabad watched an "AI-powered" trading app turn his deposits into a small fortune, at least on the screen. Each week the number climbed. When he finally tried to withdraw, the platform wanted a fee first, then another, then went quiet. By then he had lost more than $275,000. His mistake was not greed or stupidity. It was trusting a dashboard.

You have seen the ad that feeds platforms like his. Maybe halfway through a YouTube video, maybe sandwiched between two real stories on a crypto news site. A confident voice, often cloned, sometimes wearing a face you recognise. The pitch barely changes.

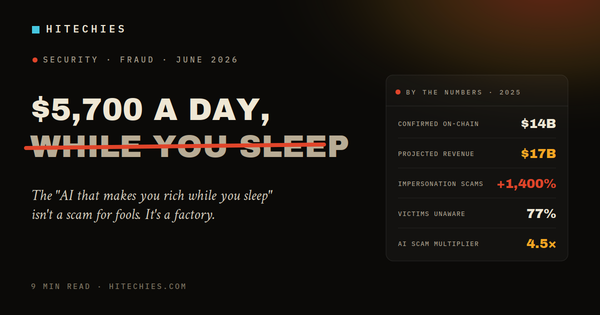

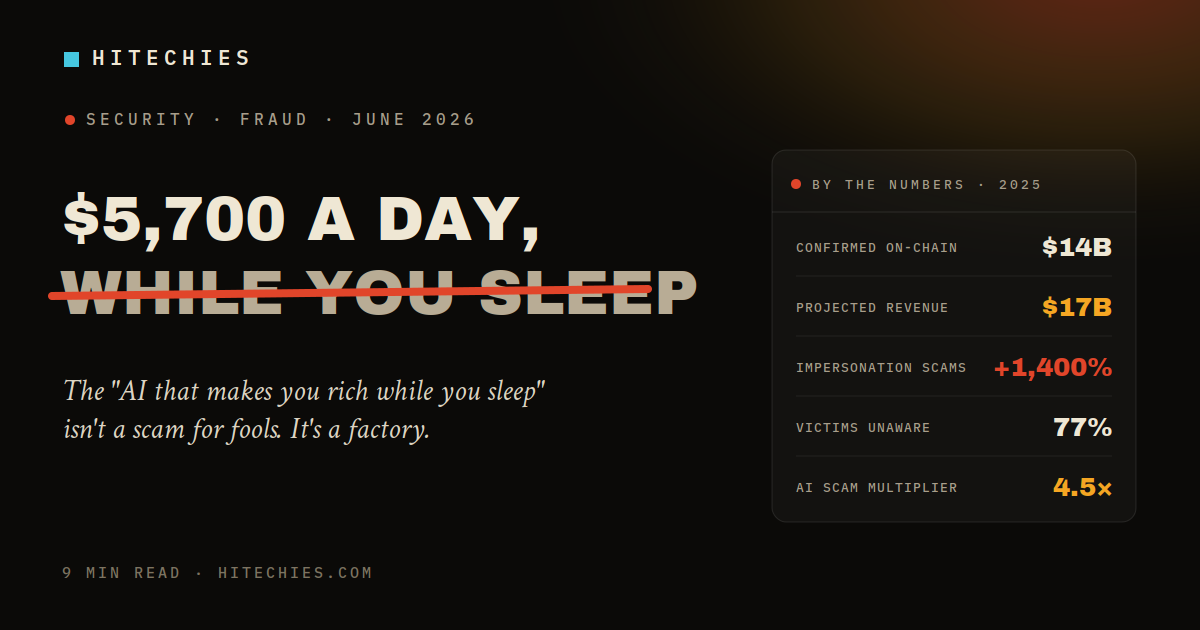

Australia's securities regulator, ASIC, quoted almost exactly that script in a 2026 warning. It is not a one-off. It is a template, running in dozens of languages, behind thousands of near-identical landing pages. The number on the screen changes. $1,500 a day. $5,700 a day. Whatever tests well. Understanding the mechanics underneath matters, because by the authorities' own tallies this is now one of the largest fraud categories on the internet by reported losses.

A note before the numbers, because it matters for everything below. The problem here is not AI, and it is not automated trading as a concept. Both of those can be entirely legitimate. The problem is fraudulent marketing wrapped around a platform that does not do what it claims. I'll come back to that distinction, because it is the whole game.

The numbers, and where they come from

Start with scale, because the scale is the part people get wrong. This is not a handful of sad stories.

The FBI's Internet Crime Complaint Center (IC3) reported a record $9.3 billion in cryptocurrency-related fraud losses for 2024, up roughly 66% on the year before, with investment fraud the largest single category.

Narrow it to the cyber-enabled investment fraud that scammers themselves call "pig butchering," and the trend is steeper still. The same FBI reporting shows losses rising from about $3.96 billion in 2023, to $5.8 billion in 2024, to more than $7.2 billion in 2025, the last figure drawn from the FBI's IC3 2025 annual report published this spring. Those are floor numbers, not ceilings, because the FBI is explicit that most victims never report.

Blockchain analytics firm Chainalysis, in its 2026 Crypto Crime Report, confirmed at least $14 billion in scam inflows on-chain for 2025 and projected the total to climb past $17 billion as more illicit wallets are identified. The wording matters: the $17 billion is estimated scam revenue, not a confirmed loss total, and the two are not the same thing. The same report found impersonation scams grew more than 1,400% year over year, the average scam payment jumped from $782 to $2,764, and scams with on-chain links to AI tools pulled in roughly 4.5 times more revenue per operation than those without.

Every figure above is linked to its source. Check them. That is the standard this topic deserves, and the standard most of the ads you'll see fail instantly.

Who actually loses

The picture of the victim is usually wrong. People imagine someone careless or greedy. The data points elsewhere.

Older people lose the most in absolute terms. Per the FBI's IC3 figures, Americans over 60 reported around $2.8 billion in crypto-crime losses in 2024, more than any other age group. But the funnel catches the young and the financially literate too, because it is not built to fool foolish people. It is built to fool patient, hopeful, sometimes lonely people, which at some point describes most of us.

The Hyderabad businessman from the opening was not an outlier. The same Times of India reporting describes a 79-year-old woman in Bengaluru losing around ₹35 lakh (roughly $42,000) to a near-identical setup. Different ages, different cities, identical arc: profit on the screen, a wall at the exit.

And the scale is not anecdotal. In what the Metropolitan Police call the world's largest cryptocurrency seizure, UK authorities recovered about 61,000 bitcoin from Zhimin Qian, also known as Yadi Zhang, tied to an investment fraud that, by police accounts, defrauded more than 128,000 victims in China between 2014 and 2017. She was later sentenced to over 11 years. A single fraud, a six-figure victim count. The individual stories are just the part you can see.

The FBI's victim-outreach programme, Operation Level Up, surfaced the detail that stays with you. Of the people they reached while the scam was still running, 77% had no idea they were being defrauded. They thought they were winning. The same programme has referred dozens of victims to specialists for suicide intervention. That is the real texture underneath the cheerful ad.

The part that needs saying: AI investing is not the scam

Here is where a lot of warning pieces overreach, so let me be precise. Automated and AI-assisted investing is a real, legal, regulated industry. Quant funds have existed for decades. Registered investment advisers use machine learning. Licensed brokers offer algorithmic tools. Copy-trading and portfolio bots can be perfectly legitimate. Saying "AI trading" and "scam" in the same breath, every time, is guilt by association, and it is wrong.

It is more useful to think in three buckets.

Legitimate, regulated tools. They show real performance history including the bad periods, publish drawdowns and risk profiles, are transparent about custody and fees, keep you in control of withdrawals, and let you use trade-only API keys so the tool can trade but never move your coins out. They never promise a fixed daily return, because no honest system can.

Genuinely speculative products. Real, but high-risk and often badly performing. You can lose money here too, but you can verify the assets, withdraw freely, and read the risks. This is risk, not fraud.

Outright fraud. No real trading, a dashboard the operator edits by hand, and an exit that never opens. This is what the rest of this article is about.

The line between bucket three and the other two is not the word "AI." It is three things: a guarantee of returns, an inability to independently verify that your assets exist, and restrictions when you try to withdraw. Hold those three tests in your head and most of the confusion disappears.

If you are weighing an actual automated or AI-assisted platform, five questions sort most of it out:

- Who holds custody of the assets, you or them?

- Can you withdraw any amount, any time, with no surprise fee or hold?

- Is the performance independently audited, with the losing periods shown, not just the wins?

- Is there a named, regulated entity behind it, in a jurisdiction you can actually check?

- Can you restrict the platform's API access to trade-only, so it can never move funds out?

A legitimate operator answers all five plainly and in writing. A scam dodges at least one, usually the first or the second.

How the fraud funnel works

The fraudulent version has a shape. The dominant pattern, the one the FBI and Chainalysis describe as pig butchering, runs in five moves. It is not the only structure out there. Fake exchanges, Telegram pump groups, forex clones and pure romance scams all exist and vary. But this funnel is the template the big operations run, so it is the one worth knowing cold.

To make it concrete, follow one person through it. The following composite combines details from several documented fraud cases. It is not one real person, but every beat below is taken from real ones.

She is in her early sixties, newly retired, careful with money. A warm message lands in a hobby group: a member has been quietly earning a second income from an AI trading app. There is a free session, a patient mentor, screenshots of other people withdrawing. She deposits $500 to test it. Within a week the account balance is up, and she withdraws $120 cleanly. That small, successful withdrawal is the moment the trap closes, because now she has proof. Over three months she moves in $40,000 and watches it "grow" past $90,000 on a screen the operator controls. When she tries to cash out, a tax appears: pay 15% first, then the funds release. She pays. The balance climbs again. Then the app stops loading and the mentor is gone.

Now here is that same story, taken apart into its moving parts.

The hook. An ad, a DM, a wrong-number text that turns friendly, a dating-app match, a comment in a Telegram or WhatsApp group. The entry point looks like luck. It is volume. Millions go out; a tiny hit rate pays.

The warm-up. Nobody asks for money yet. First comes attention. A mentor, a friendly community, screenshots of other members cashing out, a free starter session. This can run for weeks. The crews call this fattening the pig. The whole category takes its name from Chinese criminal slang, shā zhū pán, as Chainalysis documents: find the pig, fatten it, then slaughter. They use that word for the victim, internally, on purpose.

The small win. You deposit a modest amount. The dashboard lights up green. Crucially, you may be allowed to withdraw a little early on. That small successful withdrawal does more work than any sales pitch, because it converts a skeptic into a believer. You now have proof. Except the proof is a number the operator controls.

The escalation. The balance climbs fast. There is a limited window, a bonus tier, a pool closing soon. You move more in. Maybe you borrow. The fake profits compound beautifully on a platform that is rendering pixels.

The slaughter. You try to withdraw the big balance. Now there is a tax to pay first. Or a fee. Or a hold that clears once you deposit a little more. Every fix is another extraction. Then, when you run dry or catch on, the platform and the mentor vanish together.

Why the dashboard is the whole con

This is the technical heart of the fraudulent platforms specifically, and it is simpler than people expect.

These platforms are usually not broken trading systems, and often not trading at all. In the fraud cases investigators have unpicked, the "platform" is a website with an admin panel, and the operator sets the numbers you see. Your balance, your daily return, your portfolio: a content management system with a finance skin.

This is why the fake profits look so clean. Real markets are ugly. They gap, stall, and bleed for days. A genuine system has drawdowns and bad weeks. These fake platforms rarely do, because losses hurt retention. You are not looking at a market. You are looking at a scoreboard the other side is allowed to edit, and the only real transaction is the one moving your deposit out the door. The FBI's description of these schemes is blunt: in reality, all victim funds flow directly to the scammers. From there, Chainalysis's 2026 Crypto Crime Report documents the money moving through professional laundering networks that increasingly avoid regulated exchanges, likely because exchanges can freeze funds.

So the test for a real platform is never the dashboard. It is whether money comes back out, in full, without a new fee appearing. Everything else is theatre.

Why AI made the fraud cheaper

These scams predate generative AI. What plausibly changed is the cost of running one convincingly. I'll flag that as the likely mechanism rather than a proven one, because the public data shows correlation and effect more clearly than a clean causal chain.

The pieces are easy to see. Voice cloning lets a "mentor" sound like a trusted broadcaster for the price of a subscription. Deepfake video lets a celebrity appear to endorse a platform in an ad that took minutes to make. Language models turn the romance-scam messages, once clumsy and full of tells, into warm, fluent text in any language, around the clock, across hundreds of targets at once. Chainalysis attaching a 4.5x-per-operation figure to AI-enabled scams is the strongest single data point that this is not just vibes. It still does not fully separate AI's effect from rising crypto adoption, and I won't pretend it does.

This is the same double edge I wrote about in the $10.5 trillion problem: AI arms the attacker at least as cheaply as it defends the target. And the operations are run like businesses, with scripts, shift rotas and CRM software to track victims. Crime adopted the SaaS playbook: buy the kit, rent the infrastructure, plug in.

The darkest documented part is the labour. The October 2025 federal indictment tied to a $15 billion bitcoin seizure accused Prince Holding Group of running forced-labour compounds in Cambodia, where trafficked people were held and made to run these scams. So the fluent, patient message on your screen may have been written by someone being coerced. The person on your end and the worker on the other end can both be victims of the same machine.

The ten-second test

You do not need to be technical to catch these. You need a short checklist and the discipline to walk away. If a pitch trips even one of these, treat it as fraud until it proves otherwise.

- It promises a fixed or daily return. "$5,700 a day," "guaranteed 3% daily," "risk-free arbitrage." No real market does this. A line that never has a bad day is fabricated.

- A face or a guru is doing the selling, not verifiable performance. Celebrity endorsements, AI-generated news pages, "I got rich, now I'll teach you." Real tools show audited metrics and drawdowns. Fraud shows vibes.

- There is urgency. Countdown timers, "spots closing tonight." Pressure exists to stop you checking. Legitimate things survive you sleeping on it.

- You were contacted out of nowhere. A wrong-number text, a flattering DM, a new friend who pivots to investing. Cold contact plus money is the oldest signal there is.

- Withdrawals come with conditions. A tax, a fee, a deposit before you can cash out. Real platforms never ask you to deposit in order to withdraw.

- You cannot independently verify the assets, or you had to hand over custody. If the only evidence your money exists is a dashboard the operator controls, you don't have assets. You have a screenshot.

The simplest version of all of it: if you cannot withdraw a small amount cleanly today, the big balance is not real. Test the exit before you trust the entrance.

The second slaughter

There is a cruel epilogue. After the scam collapses, a second wave often arrives. A "recovery" service, a "blockchain forensics" firm, sometimes someone posing as an official, contacts the freshly drained victim and offers to get the money back. For a fee, naturally.

Often it is the same crews, or crews who bought the victim list, hitting the same people again, this time selling hope instead of greed. Treat any unsolicited offer to recover lost funds, especially one wanting payment upfront, as part two of the original fraud. Real recovery is rare, slow, and runs through banks, exchanges and police, not through a confident stranger in your inbox.

If you are in one right now

Stop depositing immediately, including the "one last fee" to unlock a withdrawal. That fee is not a bridge to your money. Screenshot everything: the platform, the chats, the wallet addresses, the transaction IDs. Then report it. In the US, file with the FBI at ic3.gov and the FTC at reportfraud.ftc.gov. If you sent funds through a regulated exchange, contact its fraud team fast, because receiving addresses can sometimes be flagged. Tell your bank. Tell someone you trust out loud, because shame is what keeps people paying, and saying it breaks the spell.

You are not stupid for getting caught. The operation is engineered by professionals, increasingly with AI doing the heavy lifting, to bypass the part of your brain that knows better. Most of the people the FBI reached did not even know yet. That is the design.

The takeaway

Crypto being volatile is a separate and legitimate conversation. I've written before about how the wild west of DeFi is slowly maturing. And to be fair to the technology, plenty of regulated firms use AI in investing responsibly. None of that is what we're talking about here.

What separates the fraud from the real thing is not the word "AI." It is the guarantee of returns, the inability to independently verify your assets, and the wall that appears when you try to withdraw. Anything carrying all three is not a risky investment. It is a screen showing you a number while a wallet empties into another country.

So the rule is short enough to remember at 1am, which is exactly when these ads find you. Nobody builds an AI that prints money and then hands it to strangers through a Facebook ad. If the returns are guaranteed, the only guaranteed thing is who keeps the money. It will not be you.