I went to Money20/20 Europe expecting the usual hype. What I got was the sound of an industry that has stopped debating the future and started wiring it up — with the caveat that a conference is the most biased room you will ever stand in.

I was at the RAI in Amsterdam for Money20/20 Europe, June 2 to 4. The photos I took mostly look like every other year. Lanyards, coffee queues, tote bags nobody will use again. What actually changed was the talking.

For years this show ran on hype. Who's the next disruptor, who just raised, who's finally going to eat the banks' lunch. This year the room felt flatter and more serious, and I think that's because the big questions quietly stopped being questions. Nobody on the stages I sat in front of was arguing about whether AI would handle payments, or whether stablecoins were real money. They had moved on to the boring, expensive part. Who builds it. Who's liable when it breaks. Who gets paid.

About 7,400 people came, from more than 100 countries, and the organizers kept reminding us that one in three was C-suite. The four official themes were AI and the Agentic Age, The Great Rebundling, Money Stack Rewired, and Regulation in the Fast Lane. You can read those as marketing. But the companies pushing them weren't startups in the cheap seats. They were Mastercard, Visa, Fireblocks, Coinbase, Stripe, Circle. The incumbents have stopped watching and started shipping, and that was the real headline of the week. How much of that shipping turns into anything is a question I'll come back to, because it's the one the room is least keen to answer.

01 / Agentic AIWhen every action becomes a line item

Agentic AI was the loudest thing in the building. Arjun Sethi, Kraken's co-CEO, was into it within minutes of the opening keynote. The framing has shifted, though. Last year people were demoing chatbots that could tell you your balance. This year they were demoing software that goes and does the thing for you. Finds the product, picks it, pays for it, with you nowhere in the loop.

The card networks are not letting that happen to them. Mastercard has Agent Pay, where an agent has to be registered and verified with what they call an agentic token before it's allowed to spend a cent. Visa built its own flavour, Intelligent Commerce. Stripe wired both of those into its Agentic Commerce Protocol and bolted on Klarna and Affirm for buy-now-pay-later. Google has a protocol. AWS shipped one running on Coinbase's x402. Everybody wants to be the layer the agents have to authenticate through, because that layer is where the money and the control sit.

Some of it is live, not slideware. Earlier this year Mastercard and Santander ran Europe's first real end-to-end payment made by an AI agent inside a regulated bank. That one happened. The forecasts around it I'd treat more carefully. McKinsey keeps repeating that agents could be moving three to five trillion dollars of consumer spending by 2030, a figure quoted on stage so often it started to sound like a chant. Salesforce reckons AI already nudged something like 67 billion dollars of orders during last year's Cyber Week. Both numbers are softer than they look. Nobody was clear on how much of that is an agent genuinely deciding and paying versus a human clicking buy after an AI suggested something, and that gap is doing a lot of quiet work in those headline figures.

There's a thread running under all of this that I don't think the payments crowd has fully clocked, because it shows up more clearly on the software side.

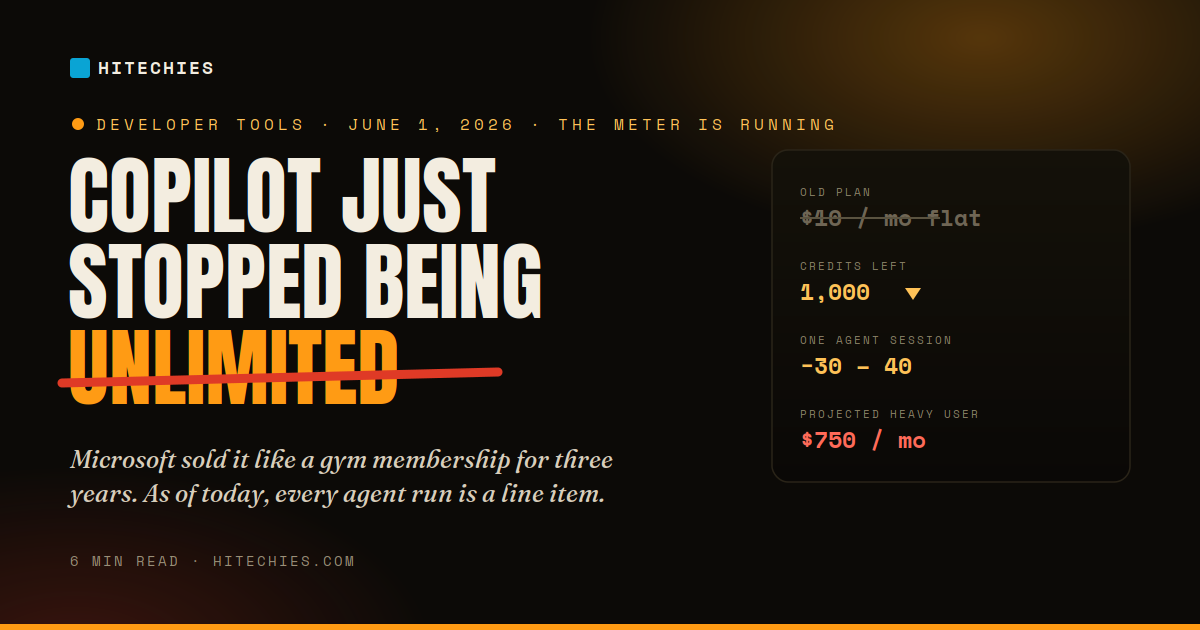

The card above is about Copilot, not payments, and I should be honest that the economics aren't identical. Microsoft meters Copilot because inference costs real money per call. Payments get metered because risk and compliance and settlement cost money. Different drivers. But the shape that falls out is the same. Once an agent is firing off hundreds of small calls to finish one task, flat-rate pricing falls apart. You can't sell unlimited when every run costs you something, so Microsoft put a meter on it. The infrastructure people in Amsterdam are building the payments version: rails that can settle tiny amounts instantly, agent to agent. The old card-and-bank setup was designed for a human standing at a checkout, happy to wait two days for the cash to clear. Agents don't stand around.

The risk side got real too. A person logs in once and buys one thing. An agent gets handed the keys and keeps acting, across lots of merchants, for as long as you let it. So if someone gets into the agent's brain rather than stealing a single card, they don't get one bad charge. They get the whole stream. Chargebacks turn strange as well. The old question was whether the customer meant to buy this. The new one is whether you can prove the agent was authorized to. A few speakers were refreshingly blunt that the technology is ready and the rulebook isn't, and that gap is the thing I'd keep an eye on.

02 / Money Stack RewiredThe giants go all-in on stablecoins

If agents are what's spending the money, stablecoins are increasingly what the money is made of. The show called this Money Stack Rewired. In plainer English: stablecoins quietly turned into settlement infrastructure while everyone else was busy arguing about Bitcoin, and in 2026 the big networks finally admitted it out loud.

The volume is why. McKinsey and Artemis put real stablecoin payment flow at around 390 billion dollars last year, roughly double the year before. Worth saying plainly: most of that is still treasury, liquidity and cross-border movement between businesses, not your nan buying milk. Mastercard walked into Amsterdam off the back of its Crypto Partner Program, which has roped more than a hundred crypto firms, fintechs and banks onto its rails. The partner list is genuinely something: Binance, PayPal, Ripple, Circle, Crypto.com, SoFi, Worldpay, and on it goes. It's pointed at cross-border transfers and business payouts, running across Solana, Polygon and a handful of other chains.

What stuck with me was who Mastercard handed the scary parts to. Custody and compliance on that program run through Fireblocks and BitGo, with Chainalysis watching the transactions for anything dodgy. The second-biggest card network on the planet did not build its own crypto security. It rented it.

Fireblocks had one of the better sessions of the week, with a lot less hype than most. Michael Shaulov, the CEO, sat down with Elliptic's Simone Maini to talk about institutional crypto in Europe, and his point was basically that banks have stopped asking whether digital assets matter and started asking how to plug them in without getting burned. Checkout.com made it concrete with a stablecoin acceptance feature built on Coinbase Payments, plus a Fireblocks deal that lets a US merchant get paid into a stablecoin wallet around the clock instead of waiting for banking hours. MoneyGram launched its own dollar stablecoin, MGUSD, on Stellar. Visa kept widening USDC settlement, with Circle sitting under a lot of it.

One thing the show's stablecoin enthusiasm glossed over: stablecoins are only one branch of digital money. A fair few of the banks in the room are quietly building tokenized deposits and wholesale CBDCs at the same time, the regulated cousin of the same idea, and they are not all betting the same way. The settlement layer of 2030 might be stablecoins. It might be tokenized bank money. Amsterdam was loud about the first and oddly quiet about the second.

Money20/20 even gave this a physical home this year, a zone called The Intersection where the trad-finance suits and the crypto crowd were supposed to mingle.

When MoneyGram, Checkout.com, both card networks and the biggest custody shop are all shipping stablecoin product in the same three days, the debate over stablecoins as settlement plumbing looks close to settled. Whether ordinary people ever knowingly pay in one is a separate question, and the honest answer right now is mostly no.

03 / The Great RebundlingThe giants are buying, and Europe is uniting

For about a decade the move in fintech was to unbundle the bank. Take one annoying thing a bank does, do it ten times better, peel off that slice and build a company on it. The Great Rebundling is the show admitting that era is done. Customers got sick of stitching a dozen apps together, so the game now is putting it all back into one place, and the fast way to do that is to buy the pieces you're missing.

The deals tell the story. Global Payments bought Worldpay for 24.25 billion dollars. Mollie bought GoCardless for just over a billion euros. A lot of this is incumbents buying their way out of years of accumulated technology debt, and more than one panel said exactly that without much spin.

The rebundling story I keep thinking about isn't a takeover, though. It's political. Before the show, the Wero initiative, the bank consortium out of France, Germany, Belgium and the Netherlands, tied up with the EuroPA group, which brings in Bizum in Spain, Bancomat in Italy, Vipps across the Nordics and SIBS in Portugal. Between them they're claiming something like 130 million users across 13 countries, all running on Europe's instant-payment rails. The whole point is to let a Spaniard pay a German straight from their normal banking app and never once touch Visa, Mastercard or PayPal. People are openly calling it payment sovereignty now. Europe has decided it would rather its money didn't move on American wires, and that decision was sitting quietly underneath a lot of the polite conference chat.

On day one the UK got a brand-new payment scheme, UKPI, its first in nearly twenty years, going back to Faster Payments. GoCardless and a few others spent the week selling account-to-account rails that run straight over open-banking APIs and skip the card networks and their fees altogether. The clever part of the pitch was that those same rails are what agentic payments are going to need anyway, since they're API-first and settle in real time. The rebundling story and the agent story keep turning out to be the same story.

04 / Regulation in the Fast LaneCompliance as the moat

The theme nobody wants at the party is regulation, and this year you couldn't get away from it. Europe's pipeline is a wall of acronyms. PSD3, the Instant Payments Regulation, FiDA, DORA, the AML package, MiCA, the EU AI Act, plus national e-invoicing rules. Most of it is landing now rather than someday. AI Act enforcement starts ramping in August. The US is off doing its own thing with the GENIUS Act on stablecoins, and the gap between the two regimes came up over and over. Build for MiCA over here, build for GENIUS over there, and good luck getting them to agree.

The smarter players had already baked this in. Mastercard's crypto program was built to sit inside MiCA and the US rules from the start, and they pitch that compliance as a feature rather than a cost. I think they're right, annoyingly. When agents are moving money on their own and stablecoins settle in seconds, being the option a regulated bank can actually say yes to is worth more than being the cheapest one in the room. The firms treating regulation as a design constraint are the ones with live product. Everybody else is building fast and hoping the rules show up before the lawsuits do.

05 / The Other SideHow much of this is actually shipping?

Here's the part a conference makes it easy to forget. I spent three days in a building full of people who are paid to believe this future arrives on schedule. Fintechs, payment firms, crypto shops, infrastructure vendors. Everyone on stage is selling the thing they need investors to fund. A bank CFO or a regulator walking the same floor would tell you a flatter, more cautious story, and they wouldn't be wrong to.

Fintech has a graveyard of trends that looked just as inevitable from a stage. Facebook's Libra was going to remake money. The metaverse was going to host payments. BNPL was going to become a super-app. Open banking was going to change how everyone paid, years before it actually moved the needle, and in plenty of markets it still hasn't. A fair amount of what got announced this week will do real volume. Some of it will quietly do almost none, and you won't see the follow-up press release.

The thing conferences underrate most is people. Consumers do not care about settlement rails or custody or interoperability. They care about whether the thing works and whether it's annoying. Faster payment rails have existed for years in some countries without changing how anyone actually pays. Better infrastructure does not automatically drag demand along behind it.

And the tidy story, AI then stablecoins then rebundling then regulation then the future, only holds if nothing big breaks. Plenty could. One serious agent-fraud incident, where a compromised orchestration layer drains real money, would freeze every bank's agent rollout overnight. A stablecoin depeg at the wrong moment would do the same to settlement. An AI liability case with no clear answer on who pays would scare off the cautious majority. MiCA or the AI Act enforced harder than expected could stall the lot. Any one of those resets the timeline by a couple of years.

So read everything above as the optimistic version. The one the room wanted me to leave with.

06 / The ReadWhere we're heading, if it holds

Step back from the four themes and they're pretty obviously one thing wearing four different lanyards. The bet on stage is that agents end up running inside the rebundled super-apps, on top of stablecoin or tokenized-deposit rails, watched over by regulators finally moving at something close to the speed of the market.

The part that surprised me was the power map, though I'd hold it loosely. The easy read is that the card networks aren't getting disrupted this time, they're doing the disrupting, bolting agent frameworks on top and renting their crypto guts from Fireblocks, Chainalysis and BitGo. I half believe that. The other half remembers that A2A rails, Wero and the instant-payment schemes exist specifically to route around Visa and Mastercard and their fees. If those win, the networks don't get to own the agentic future. They get bypassed by it. The honest version is that the incumbents are moving fast and spending hard to make sure the rebundled, agent-driven world still runs through them. Whether it works is not decided.

I'd be careful with the infrastructure story too. When Mastercard's stablecoin program runs on Fireblocks, that's worth noticing. But AWS hosts half the internet without running those companies, and a custody vendor is closer to that than to a kingmaker. Call it operational leverage, not control. Still, it's leverage the card networks chose to buy rather than build, and that choice says something.

My read, for whatever it's worth. Money is turning programmable and self-driving, and the fight from here is mostly about plumbing. Whose rails it runs on, and who holds the keys and the audit trail when an agent does something it shouldn't. The giants have worked out that owning a slice of that is worth more than owning a thousand shiny consumer features, which is why they're spending the way they are.

Which brings me back to that meter. Whether you're a developer watching your Copilot bill turn into a per-run tab, or a shop getting paid by some customer's AI in stablecoins at two in the morning through a Mastercard partner running on Fireblocks, the rule is the same. Every action gets a price, a record and a rail attached to it. Amsterdam wasn't a preview of that world so much as the year the biggest names in money decided to go and build it, meter and all. Whether they get there on their schedule, or get bypassed by the rails trying to route around them, or get knocked back by one bad year, the show couldn't tell me. The direction I'd put money on. The timing I'd leave on the table.